We are excited to announce our integration with QuantConnect! This offering empowers users with state-of-the-art research, backtesting, parameter optimization, and live trading capabilities, all fueled by the robust market data APIs and WebSocket Streams of Polygon.io.

QuantConnect provides one of the most sophisticated open-source algorithmic trading platforms in the world, along with the cloud infrastructure needed to create, evaluate, and deploy trading strategies at scale with unprecedented efficacy. Recently, the QuantConnect team launched support for using Polygon’s data APIs directly in their cloud, on-prem, and open-source platforms. This powerful combination gives researchers unmatched ease to design and execute winning algorithms with high-quality data.

At the core of QuantConnect’s platform is Lean, an open-source engine built in C# and Python, allowing quants and engineers to design, backtest, and deploy trading algorithms. QuantConnect's cloud-based IDE seamlessly integrates with Lean to provide quants with a robust platform for strategy research, development, and live trading. Lean comes packed with hundreds of technical indicators, multi-asset modeling, data normalization, and helpers for machine learning.

The Polygon integration is offered across all three of QuantConnect's platforms: a user-friendly, robust Cloud Platform where developing and deploying a live algorithm is possible within seconds, their Local Platform with on-premise institutional support, and the LEAN CLI with an open-source pip package. The integration supports US Equities, Options, and Index market data from tick-by-tick to daily aggregated candlesticks.

This integration with QuantConnect allows you to use Polygon data at each phase of the quant research cycle. With their jupyter research, backtesting, and parameter optimization tools, users can download all the data needed and prepare it for any size project. Once backtested, the plug-in streams cleaned Polygon data to your strategies in paper and production trading modes.

We’re eager for feedback from those who take advantage of this integration. To see more about the integration and how to get started, see the QuantConnect cloud documentation.

QuantConnect features compatible with Polygon.io Data APIs:

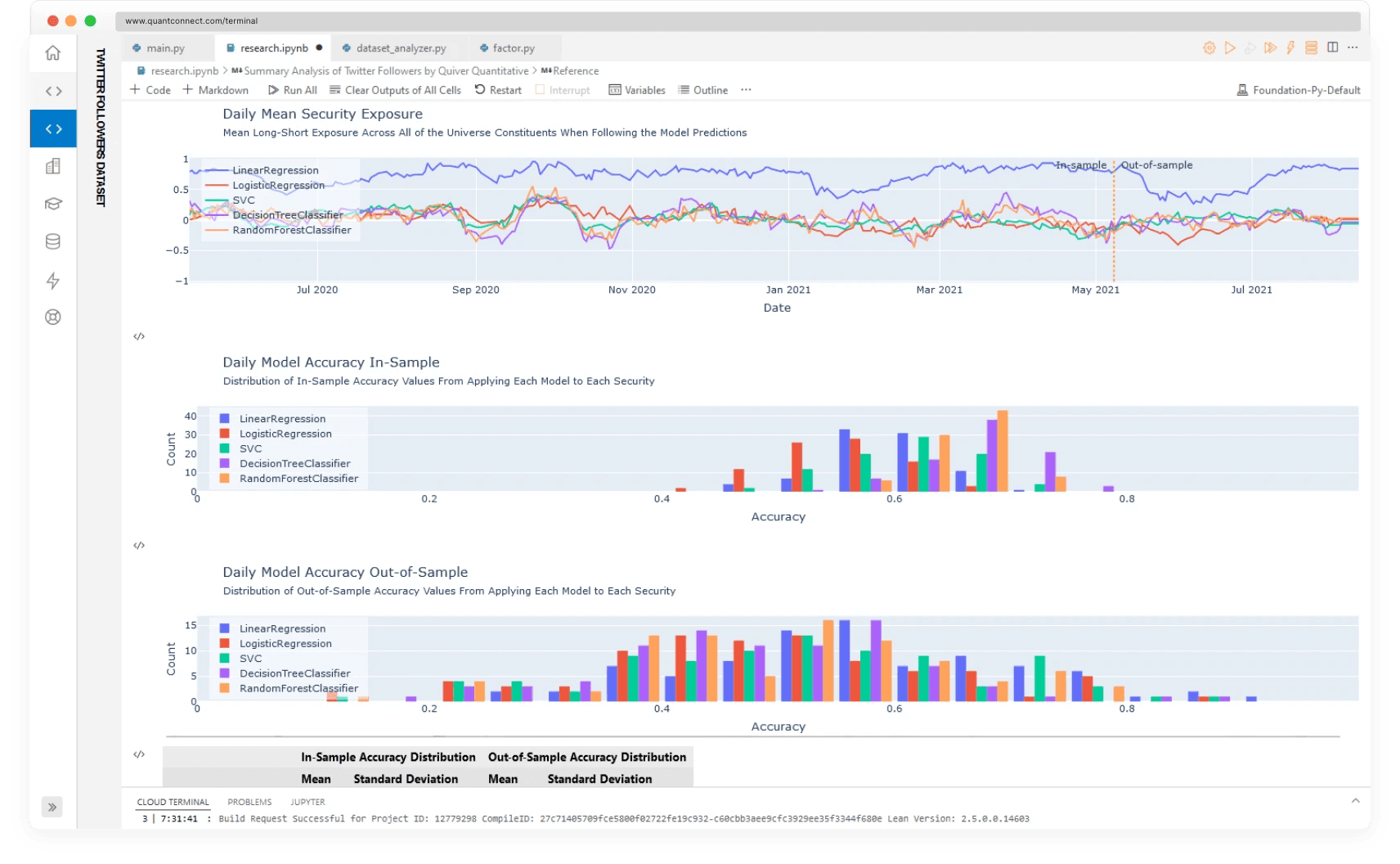

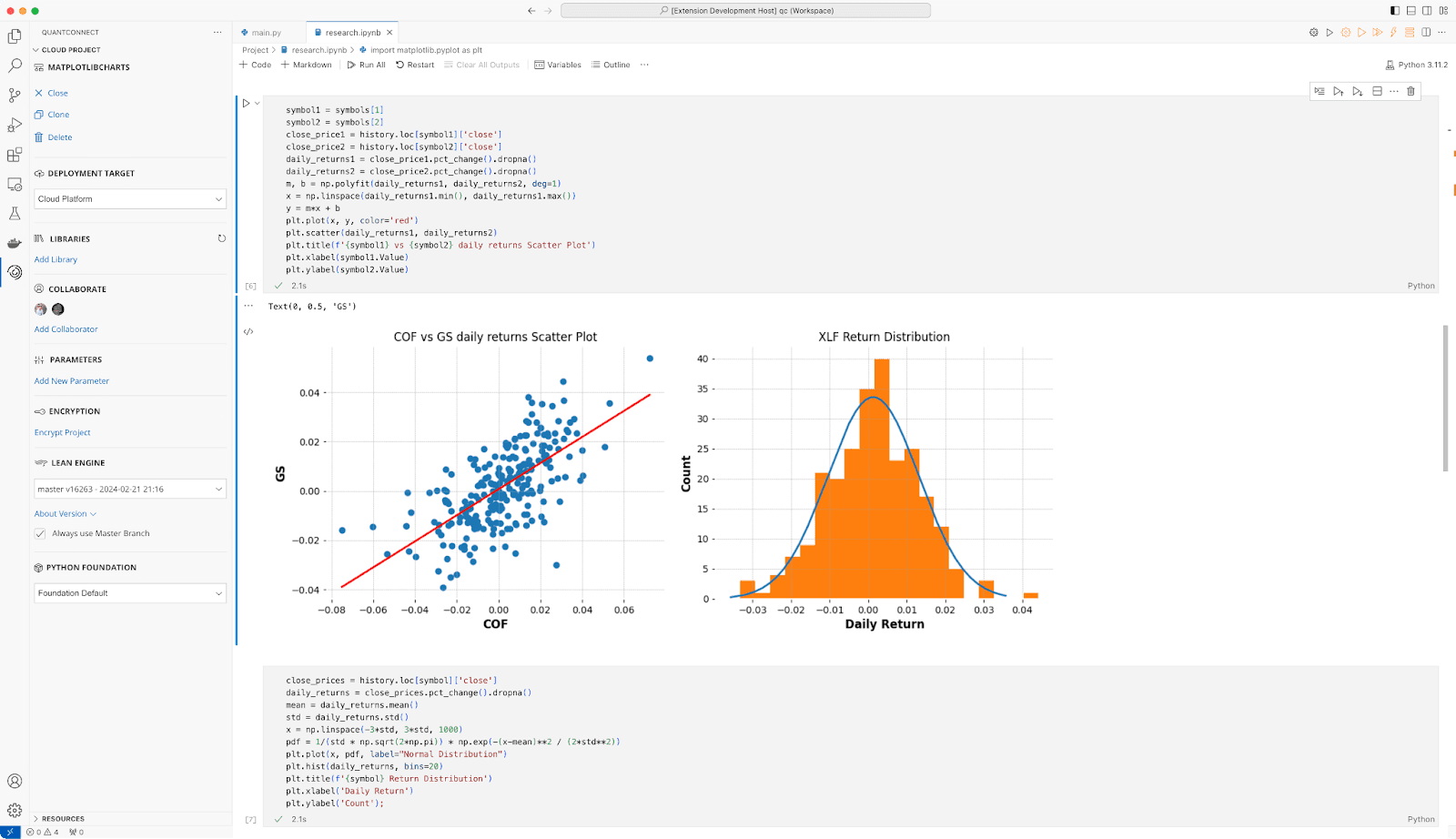

Jupyter Research Environment: Perform interactive strategy research with all the data automatically pulled from the Polygon API with the new QuantConnect integration.

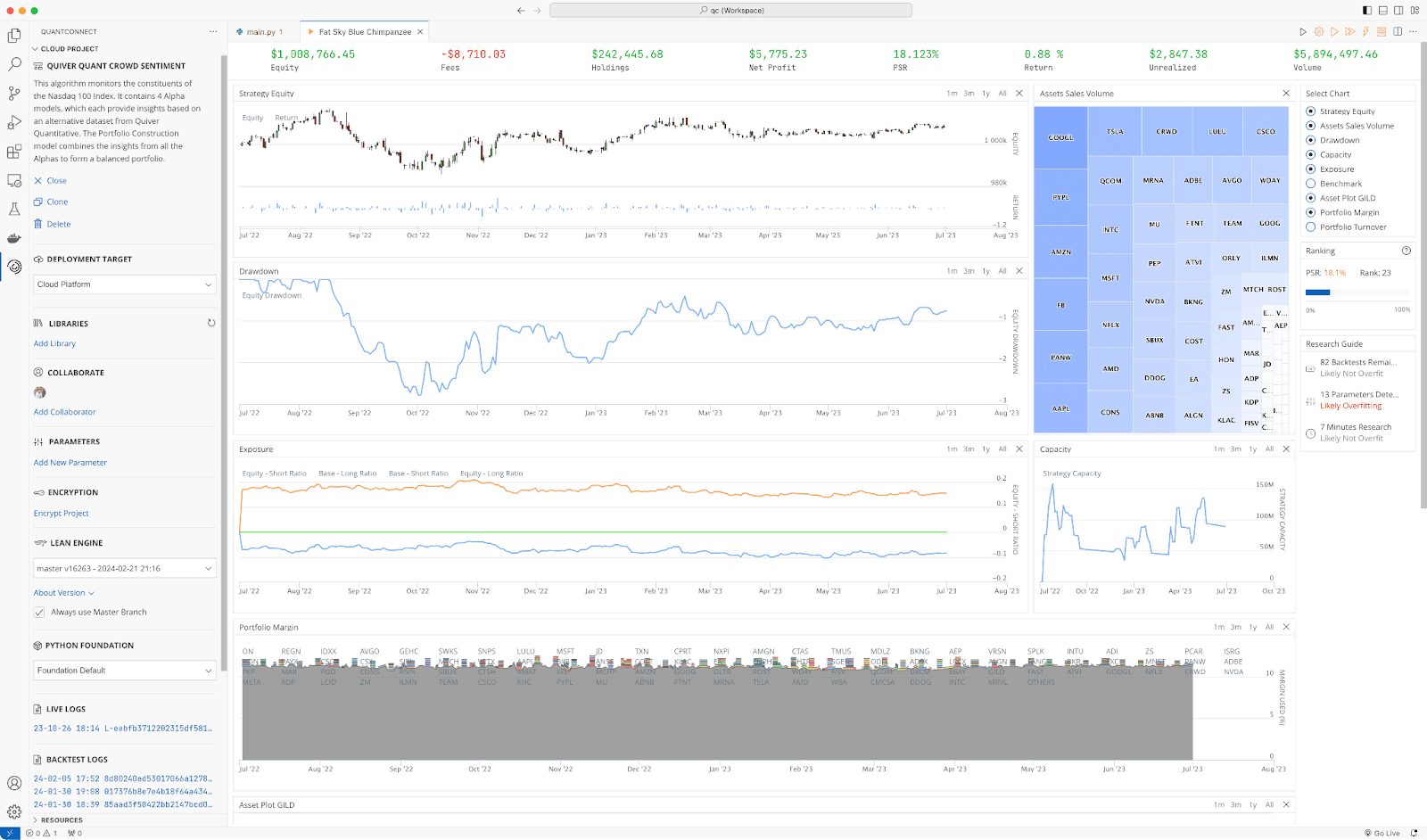

Backtesting: Quickly backtest multiple asset classes, time-horizons, with full portfolio management and margin modeling. Detailed spread, fee, and slippage models are baked in, letting you focus on your quantitative research.

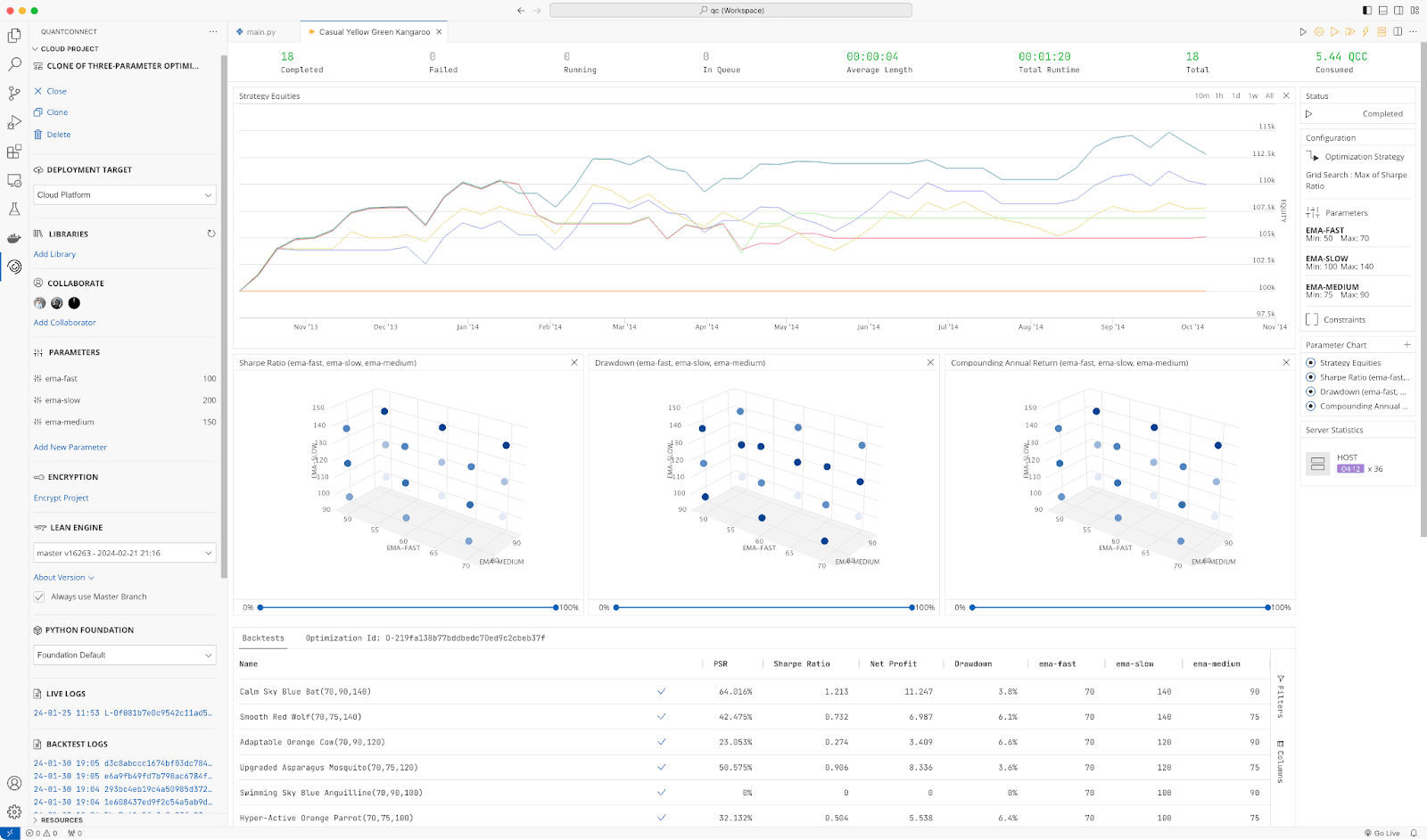

Parameter Optimization:Perform grid-search parameter sensitivity analysis to optimize ideal parameter sets for your strategy.

Hosted or On-Premise Live Trading:Once you have completed the process of backtesting and optimizing your strategies, you can seamlessly transition your portfolio into live trading mode with just a click of a button, enabling execution through your preferred brokerage provider.

Polygon.io is excited to announce a new partnership with Benzinga, significantly enhancing our financial data offerings. Benzinga’s detailed analyst ratings, corporate guidance, earnings reports, and structured financial news are now available through Polygon’s REST APIs.

This tutorial demonstrates how to detect short-lived statistical anomalies in historical US stock market data by building tools to identify unusual trading patterns and visualize them through a user-friendly web interface.